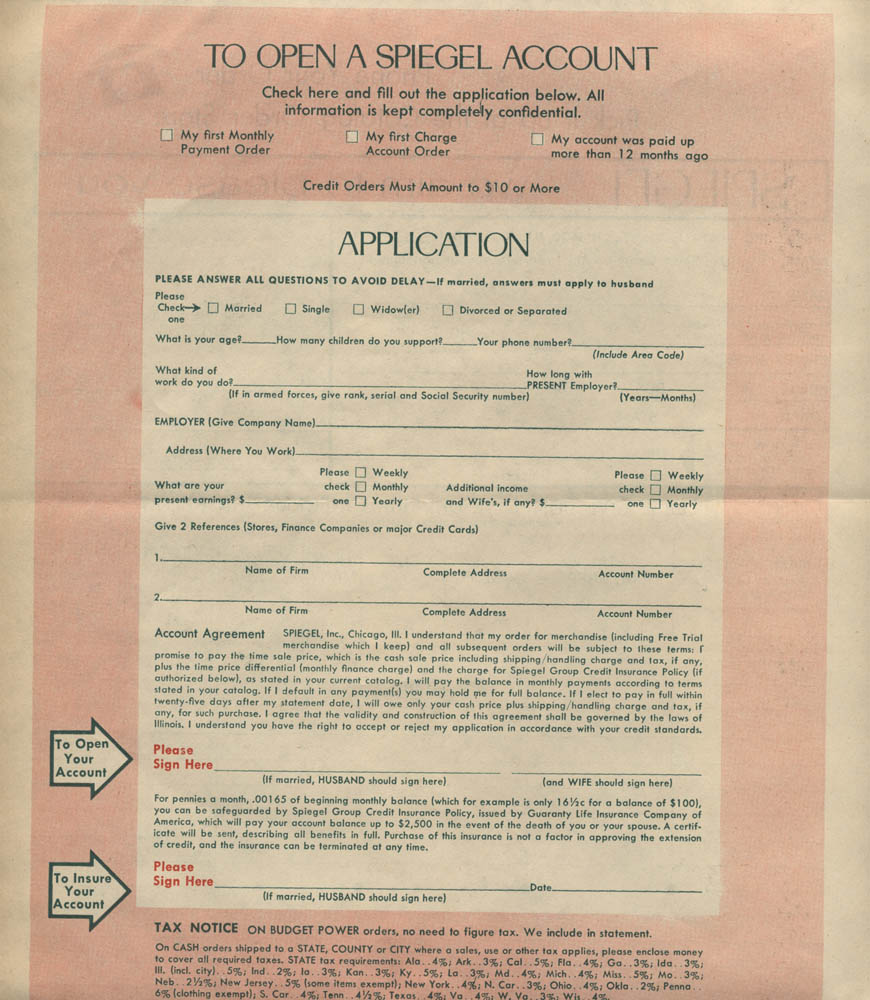

This Spiegel account application from the early 1970s is more than a piece of vintage retail paperwork. It is a window into a financial system that once treated women’s access to credit as conditional—often requiring approval from a husband, regardless of a woman’s own income, employment, or financial history.

At the center of the form is a requirement that now feels startling: if the applicant is married, the husband must sign the agreement. In many cases, the wife’s signature appears secondary. This was not unusual at the time, nor was it illegal. Prior to the passage of the Equal Credit Opportunity Act of 1974, lenders were allowed to consider sex and marital status when approving credit. Married women could—and frequently did—lose access to credit unless their husbands co-signed and accepted legal responsibility for the debt.

This requirement was not merely symbolic. The husband’s signature transferred financial liability, reinforcing the legal and cultural assumption that the husband was the “head of household.” Women were often treated as authorized users rather than independent borrowers. Even women with steady jobs and their own earnings were frequently denied credit in their own names. Divorce, separation, or widowhood could instantly unravel a woman’s financial standing, leaving her with little or no credit history of her own.

The application also highlights how invasive credit screening once was. Applicants were asked to disclose their age, number of children supported, employer information, length of employment, and income frequency. Two references—often other retailers or finance companies—were required to vouch for reliability. Credit decisions were reviewed manually and could take weeks. This friction was intentional. Credit was designed to be restrictive, cautious, and slow.

Spiegel, like many major mail-order retailers of the era, operated as both merchant and lender. Customers purchased goods on installment plans directly from the company, which functioned much like a private bank. Terms were spelled out in dense legal language, and optional credit insurance was frequently promoted, further entangling consumers in long-term financial obligations. These systems gave retailers enormous control over who was deemed “creditworthy.”

Change came in 1974 with the passage of the Equal Credit Opportunity Act, a landmark law that prohibited discrimination in credit decisions based on sex, marital status, or pregnancy. For the first time, women could apply for and receive credit independently, without a husband’s signature or approval. This shift reshaped not only consumer finance, but personal independence itself—allowing women to build credit histories, start businesses, buy homes, and control their own financial futures.

Today, credit applications are digital, approvals are often instant, and spousal permission is no longer a factor. Yet this single piece of paper captures a time when financial autonomy was restricted by law, gender, and social norms. What now seems unthinkable was once routine—and understanding that history helps explain why modern credit protections exist, and why they still matter.